Market Update for the Quarter Ending March 31, 2022

Positive March Wraps Shaky Quarter for Markets

Equity markets partially bounced back in March. The S&P 500, Dow Jones Industrial Average (DJIA), and Nasdaq Composite gained 3.71 percent, 2.49 percent, and 3.48 percent, respectively. For the quarter, the S&P 500, DJIA, and Nasdaq Composite lost 4.60 percent, 4.10 percent, and 8.95 percent, respectively.

Per Bloomberg Intelligence, as of March 25, 2022, with 99 percent of companies having reported actual earnings, the average earnings growth rate for the S&P 500 in the fourth quarter was 28.9 percent (above analyst estimates for a 19.8 percent earnings growth rate at the start of earnings season).

Technical factors were mixed at quarter-end. The S&P 500 finished the month above its 200-day moving average; however, the Nasdaq Composite and DJIA both finished the month below trend. The S&P 500 fell below its trendline at the end of February before recovering above trend in March.

International markets were mixed last month but ended the quarter in negative territory. The MSCI EAFE Index gained 0.64 percent in March but declined 5.91 percent for the quarter. The MSCI Emerging Markets Index fell 2.22 percent, capping off a loss of 6.92 percent for the quarter. The MSCI EAFE and MSCI Emerging Markets indices ended the quarter below their respective 200-day moving averages.

The 10-year U.S. Treasury yield started at 1.63 percent, increased to 1.72 percent, then surged to 2.32 percent. Short-term interest rates also experienced upward pressure throughout the quarter, driven by rising expectations for more rate hikes from the Federal Reserve (Fed). The Bloomberg U.S. Aggregate Bond Index dropped 2.78 percent for the month and 5.93 percent for the quarter.

High-yield fixed income also saw declines, with the Bloomberg U.S. Aggregate Corporate High Yield Bond Index down 1.15 percent in March and 4.84 percent for the quarter. High-yield credit spreads started the year at 3.05 percent and reached a high of 4.21 percent in mid-March before retreating to 3.33 percent at quarter-end.

Risks Change During Quarter

We saw risks to economic recovery and markets shift throughout the quarter. Declining medical risks were offset by more aggressive plans from the Fed to tighten monetary policy as well as uncertainty created by the Russian invasion of Ukraine.

Medical risks fell during the quarter when the impact from the Omicron variant peaked in mid-January before swiftly declining by quarter-end, with average daily new cases at their lowest level since last July. While additional future waves of Covid-19 are possible, the recent muted economic impact from Omicron highlights an increased ability for the economy to withstand periods of high case growth.

While we’ve made progress in controlling pandemic-related medical risks, we saw rising risks in other areas that negatively impacted markets during the month and quarter. Inflation remains high, driven by high levels of demand and supply chain shortages. Inflation levels caused the Fed to hike interest rates at their March meeting, marking the first hike since 2018.

Geopolitical risks increased during the quarter, most notably surrounding Europe following the Russian invasion of Ukraine. While immediate economic impact to the U.S. has been limited, invasion-induced uncertainty negatively impacted markets.

Economic Momentum Continues Despite Risks

Despite the shifting quarterly risk profile, economic data releases in March showed continued economic growth with last year’s positive momentum carried over. The March job report showed 431,000 jobs were added during the month, contributing to more than 1.68 million jobs created during the quarter. This impressive hiring growth helped drive the unemployment rate to a 2-year low of 3.6 percent by the end of March, signaling a strong labor market that has helped drive overall growth to start the year.

Consumer spending increased in January and February, which was an encouraging sign that consumers remain willing and able to spend. Retail sales growth was especially impressive as sales increased 4.9 percent in January and another 0.3 percent in February.

Business confidence and spending also held up well despite rising quarterly risks. Manufacturing and service sector confidence remained in healthy expansionary territory throughout the quarter. Output also showed signs of recovery, as seen by the 1.2 percent increase in manufacturing production in February.

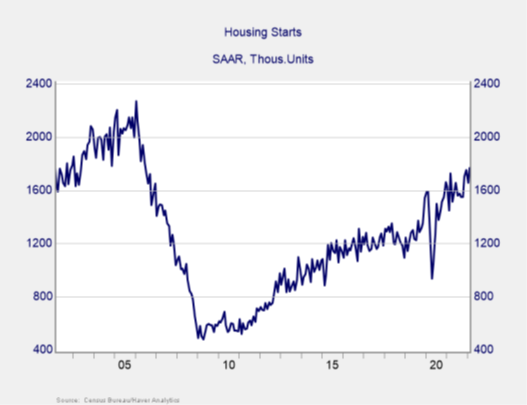

New home construction was impressive, supported by high levels of demand for housing and a shortage of existing homes for sale. As shown in Figure 1, the pace of new home construction hit its highest level since 2006 in February. The housing sector has been a bright spot in economic recovery.

Figure 1. Housing Starts, April 2002–Present

Continued Growth Expected

The first quarter served as a reminder that real risks remain despite solid medical and economic progress. The expectation for tighter monetary policy will likely continue to weigh on markets, and uncertainty from the Russian invasion of Ukraine could lead to further market selloffs if the conflict worsens.

March reports showed the economy remains on solid footing despite shifting risks. We remain in a healthy place, with impressive labor market recovery over the past two years. Businesses have shown they’re capable of operating despite headwinds created by rising rates and geopolitical uncertainty.

While negative headlines and shifting risks may lead to further short-term turbulence, strong fundamentals and continued economic recovery should help long term. Given the potential for short-term selloffs, a well-diversified portfolio that matches investor timelines with goals remains the best path forward for most. If concerns remain, reach out to your financial advisor to discuss your financial plans.

All information according to Bloomberg, unless stated otherwise.