“Always remember you matter, you’re important and you are loved, and you bring to this world things no one else can”. The Boy, the mole, the fox and the Horse by Charlie Mackesy.

I think that is such a great message for any time of year, but especially now. For me, spring signifies a time to renew, reflect and have the opportunity to refresh your mind, your body and your soul. At first glance, I thought Mackesy had written a children’s book. As I turned the pages, I realized this is a book for all of us, no matter how young or old you are.

At its core, it is a story about kindness and understanding as told through conversations between the four main characters in the title. “All four characters represent different parts of the same person,” explained Mackesy, “the inquisitive boy, the mole who’s enthusiastic but a bit greedy, the fox who’s been hurt so is withdrawn from life, slow to trust but wants to be part of things, and the horse who’s the wisest bit, the deepest part of you, the soul …”

The book is a quick read, and yet, the messages that Mackesy conveys are powerful. Be kind to yourself and to others, forgive yourself, spend more time listening to your dreams than your fears, take care of the beauty all around you, everyone gets scared but being together makes you less scared, understand that asking for help is not giving up but rather it is refusing to give up, be curious, life is not perfect and so many more lessons can be found in this delightful little book.

Mackesy was quoted as saying ‘We don’t have to pretend. We’re all the same, really. I think real closeness comes from vulnerability and the book is a journey into closeness and honesty.” I would agree. I’ll leave you with my favorite quote and sketch from The Boy, the mole, the fox and the Horse.

Market Update for the Quarter Ending March 31, 2023

Markets Rebound in March

Markets had a solid March, as a month-end rally helped bring all three major U.S. indices into positive territory for the month. The S&P 500 gained 3.67 percent while the Dow Jones Industrial Average (DJIA) increased 2.08 percent and the Nasdaq Composite notched a 6.78 percent gain. March results helped offset weakness in February and all three indices ended the quarter in the green. The S&P 500, DJIA, and Nasdaq gained 7.50 percent, 0.93 percent, and 17.05 percent, respectively, for the quarter.

These positive results came despite slowing fundamentals. Per Bloomberg intelligence, the S&P 500 average earnings decline was 2.38 percent during the fourth quarter of 2022. While this result was marginally better than the 3.26 percent decline expected at the start of earnings season, it marks the first quarter with a year-over-year decline since the Covid-19 lockdown-impacted third quarter of 2020.

Fundamentals drive long-term market performance, so the earnings decline should be monitored.

Unlike fundamental factors, technical factors were supportive for the quarter. All three major indices finished March above their respective 200-day moving averages, marking three consecutive months above trend.

International equities had a similar month to the U.S. The MSCI EAFE Index and MSCI Emerging Markets Index gained 2.48 percent and 3.07 percent, respectively. For the quarter, the MSCI EAFE gained

8.47 percent while the MSCI Emerging Markets Index gained 4.02 percent. Technical factors were also supportive for international markets with both indices finishing March above their 200-day moving averages.

Strong March for Fixed Income

Fixed income markets also experienced positive returns as falling rates supported bond investors in March. The 10-year U.S. Treasury yield fell from 4.01 percent at the start of the month to 3.48 percent at month-end. The notable drop in yields was due to increased investor demand for higher-quality fixed income due to rising concerns over the health of the banking sector. The Bloomberg Aggregate Bond Index gained 2.54 percent during the month, which contributed to the index’s quarterly return of 2.96 percent.

High-yield fixed income also had a positive month and quarter. The Bloomberg U.S. Corporate High Yield Index gained 1.07 percent during the month and 3.57 percent for the quarter. After experiencing some volatility the past three months, high-yield credit spreads ended the quarter in line with where they started this year.

Returns to highlight on this page

- Bloomberg Aggregate Bond Index: 2.54 percent in March, 2.96 percent for the quarter

- Bloomberg U.S. Corporate High Yield Index: 1.07 percent in March, 3.57 percent for the quarter

Bank Stress Worries Markets

The high-profile banking failures at Silicon Valley Bank, Signature Bank, and Silvergate Bank garnered headlines and captured investor interest in March. The initial market reaction to the bank failures was a flight-to-quality trade. Riskier assets like stocks and high-yield bonds sold off while higher-quality fixed income sectors saw yields fall and prices rise.

While regulators and insurers stepped in to ensure that depositors at these banks did not lose their deposits, the Federal Reserve (Fed) and U.S. Treasury also made capital available to other banks to reassure Americans that the banking system as a whole was healthy. The initial uncertainty caused by the bank collapses are a reminder to investors that market risks can appear at any time.

The banking turmoil in March created uncertainty and volatility, but the issues that led to the collapses appear to have been largely constrained to a handful of banks rather than a sign of systemic weakness in the banking system.

While bank health will certainly be worth monitoring in the months ahead given the Fed’s continued attempts to combat inflation through tighter monetary policy, banking system risks for investors appear to be largely behind us.

The Takeaway

- Concerns about the banking sector took center stage in

- While initial uncertainty led to an initial sell-off for risk assets early in the month, markets have since recovered as regulators and insurers stepped in to support the banking industry.

Economic Updates Positive

Despite the mid-month market turbulence caused by strain on the banking industry, economic updates released in March continued to show positive signs of growth. The February employment report displayed strong job growth, which is an encouraging sign that the labor market remains in healthy territory.

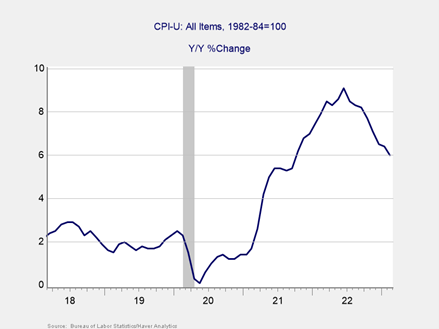

We saw continued evidence that the Fed’s attempts to combat inflation are working. As you can see in Figure 1, the year-over-year change for the Consumer Price Index fell to 6 percent in February, which is down notably from the high of 9 percent that we saw in June 2022.

While there is still work to be done to get inflation back closer to the Fed’s targeted 2 percent range, the progress that we’ve seen since peaking last summer is encouraging and signals that we’re on the right path.

Figure 1. Year-Over-Year Percentage Change in Consumer Price Index, All Urban Consumers, March 2018-February 2023

Risk Worth Monitoring

Banking-driven uncertainty in March served as a reminder that very real risks remain for markets and investors. While the worst impact from banking industry stress appears to be behind us at this time, news of additional bank weakness could lead to further sell-offs in the future. The banking system struggles also highlight the uncertainty that the Fed represents for markets and the economy, as the central bank’s attempts to fight inflation through tighter monetary policy placed pressure on banks.

Concerns about the debt ceiling and a government default linger as we get closer to a potential default in the summer or early fall. The continued housing sector slowdown also represents a possible risk for markets given the sector’s importance for the overall economy.

Looking abroad, China remains a source of uncertainty as the country’s reopening efforts have yet to be fully absorbed by the global economy. There is also potential for additional conflict from the ongoing Russian invasion of Ukraine, and it’s important to remember that unknown risks could negatively impact investors.

The Takeaway

- Banking-induced uncertainty is a reminder of

- The debt ceiling, a slowing housing sector, and international risks are key areas to monitor.

Outlook Still Positive

Despite the mid-month uncertainty, March proved to be positive for investors. While the rise in banking sector risk should be monitored going forward, developments during the month point toward contained risks at a handful of banks rather than systemic cracks in the broader banking system.

The fact that all of the major indices we track in this piece ended the month in positive territory is a good sign that markets are resilient. Additionally, the continued positive economic backdrop should help support markets in the months ahead.

The potential for further short-term uncertainty remains and a well-diversified portfolio that matches investor timelines and goals is the best path forward for most. As always, you should reach out to your financial advisor to discuss your current plan if you have concerns.

The Takeaway

- March was a positive month for markets despite rising

- Risks remain for investors and should be

- The long-term outlook is positive, with potential for short-term setbacks.