I hope that you are enjoying your summer. As many of you know, we are all avid travelers. This spring I spent a few weeks in Italy and fell in love with everything Italian– the country, the people, the food and the wine! I visited several different cities and people always ask me which one was my favorite. I’ve come to realize that it really wasn’t a particular city because they were all wonderful. What I think I will always remember are the people I met and the experiences I had. It was seeing the pride in someone’s face when they told the story of their family, their business or their town that was most interesting. It was the host of our AirBnB offering to make dinner for us and then joining us at the end of the meal with a bottle of his homemade limoncello and sharing stories that was most memorable.

We’d love to hear your travel stories and adventures! And the next time you are in the office be sure to add a pin to the map to mark the last place you went on vacation.

A gentle reminder:

We know that email and text are convenient methods of communication, and we make every effort to respond in a timely fashion. However, if you do not hear from us within 24 hours, it is likely that we did not receive your email or text. If this happens, please give us a call at the office 301.631.1207. One of us will be happy to help.

Market Update for the Quarter Ending March 31, 2023

Quick Hits

- Equity Markets Surge in June

- Fixed Income Faces Challenges

- Economy Continues to Grow

- Debt Ceiling Concerns Fade

- Market Risks Are Shifting

- Positive Outlook for Second Half of the Year

Equity Markets Surge In June

June was a strong month for equity markets as resolution of the debt ceiling impasse helped lower uncertainty and supported a risk-on environment. The positive monthly returns capped a solid quarter for stocks. The S&P 500 gained 6.61 percent for the month and 8.74 percent for the quarter. The Dow Jones Industrial Average rose 4.68 percent in June and 3.97 percent for the quarter. The technology-heavy Nasdaq Composite led the way, returning 6.65 percent in June and 13.05 percent in the quarter.

These results were supported by better-than-expected fundamental performance to start the year. Per Bloomberg Intelligence, as of June 30, 2023, with 100 percent of companies having reported actual earnings, the blended earnings decline for the S&P 500 in the first quarter was 3.1 percent. This is an improvement from analyst estimates for an 8.1 percent drop. Fundamentals drive long-term market performance, so the first-quarter data was welcomed by investors.

Technical factors were supportive for the month and quarter. All three major U.S. indices finished June above their respective 200-day moving averages, for the sixth consecutive month. The 200-day moving average is a well-known technical signal as prolonged breaks above or below this level can signal shifting investor sentiment for an index, so continued support was a positive sign.

International markets also had a positive June and quarter, but weakness in May held back quarterly returns compared to U.S. markets. The MSCI EAFE Index gained 4.55 percent for the month and 2.95 percent for the quarter. The MSCI Emerging Markets Index had a more challenging time, with the index up 3.89 percent for the month and 1.04 percent for the quarter. Technical factors for international equities were supportive in June, with both indices ending above their respective 200-day moving averages.

Fixed Income Faces Challenges

Although stocks rallied during the month and quarter, the same can’t be said for bonds. Rising long-term rates served as a headwind for fixed income investors. The 10-year U.S. Treasury yield rose from 3.61 percent at the start of June to 3.81 percent, while the Bloomberg U.S. Aggregate Bond Index lost 0.36 percent for the month and 0.84 percent for the quarter.

Yields rose in June, in part due to better-than-expected economic data. The reports are a good sign for the health of the overall economy, but they could hinder the Federal Reserve’s (Fed’s) attempts to combat inflation if economic activity stays too strong.

High-yield fixed income, which typically performs well in a risk-on environment, rallied during the month and quarter. The Bloomberg U.S. Corporate High Yield Index gained 1.67 percent in June and 1.75 percent for the quarter.

High-yield credit spreads declined for the month and quarter. Spreads dropped from a quarterly high of 4.95 percent in early May to 4.14 percent at the end of June. Falling spreads helped support a strong quarter for high-yield bonds and signal growing investor appetite for investing in higher-yielding securities.

Economy Continues to Grow

The economic updates released in June continued to show signs of a surprisingly resilient economy. The May jobs report showed that 339,000 jobs were added, which was significantly more than the 195,000 economists expected. Despite tighter fiscal conditions, businesses continued to invest and hire during the quarter. Consumer confidence and spending also improved for the month and quarter.

These positive economic updates show that the economy continued to grow in the second quarter, but the downside is that faster growth could lead to more inflationary pressure at a time when the Fed is focused on combatting inflation. While the Fed held off on hiking interest rates at its June meeting, investors and economists expect to see at least one additional rate hike of 25 basis points (bps) this year.

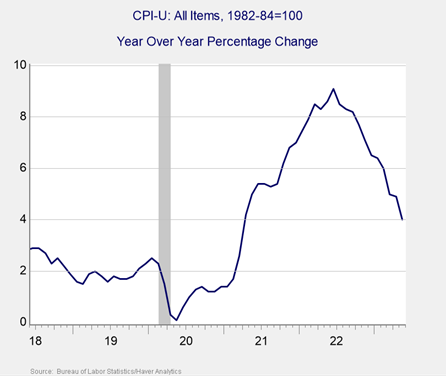

That said, we haven’t seen evidence that the positive growth in the quarter has directly caused additional inflationary pressure. The May Consumer Price Index report showed that consumer inflation on a year- over-year basis fell notably. As you can see in Figure 1, headline consumer inflation peaked at 9.1 percent in June 2022—and we’ve seen continued declines since then, ending May at 4.0 percent. Whereas this is still too high on an absolute basis, the relative improvement over the past year is evidence that the Fed’s tighter monetary policy is working.

Figure 1. Consumer Price Index, Year-Over-Year Change, June 2018–May 2023

Source: Bureau of Labor Statistics/Haver Analytics

For now, inflation and the Fed will continue to be closely monitored by investors and economists given the importance of both for markets; however, the improvements we’ve seen on the inflation front this year have been encouraging.

Debt Ceiling Concerns Fade

The debt ceiling standoff that dominated headlines and created uncertainty throughout May was successfully resolved at the start of June. The last-minute compromise to suspend the debt ceiling until 2025 effectively ensured that the economy and markets didn’t have to suffer through an unprecedented government default. This will likely become another hot button issue as we get closer to 2025, but markets reacted positively to the agreement and the worst market risks currently appear to be behind us.

As was the case with the concerns surrounding the banking industry earlier in the year, the debt ceiling standoff served as a reminder that markets continue to face real risks that can lead to short-term sell-offs. With that said, similar to banking industry concerns, the market impact from the debt ceiling standoff was limited and investors were quick to look past the brief turbulence once a deal was struck.

The Takeaway

- The debt ceiling suspension in early June helped support stocks during the month

- While the immediate market risk is behind us, risks remain and should be monitored

Market Risks Are Shifting

While the debt ceiling standoff was resolved with little lasting market impact, there are still real risks to markets. The primary risk now for U.S. investors is if inflation spikes and necessitates further rate hikes from the Fed. Although we have seen signs that the Fed’s efforts to combat inflation over the past year have been largely successful, if we do start to see a ramp up in inflationary pressure, it could lead to more hikes than investors currently expect—which could then pressure bond and stock valuations.

International risks remain as well, highlighted by the ongoing war between Russia and Ukraine and fears of a potential slowdown in the Chinese economy. While the market impact of the Russian invasion of Ukraine is largely behind us at this point, further increase in hostilities could lead to additional uncertainty and volatility.

Of course, there are also unknown risks that we can’t predict at this time, which always have the potential to negatively impact markets.

The Takeaway

- Inflation and the Fed are the primary domestic risks for the S.

- International and unknown risks should be monitored

Positive Outlook for Second Half of the Year

On the whole, the economic and market updates in June were largely positive, with better-than-expected economic fundamentals supporting market gains to end the quarter.

The economy continued to show signs of solid growth in June, as evidenced by high levels of hiring, progressing consumer confidence, and continued consumer spending growth. While inflation and the Fed are risks to monitor, we’ve already made positive progress in lowering inflation and further improvements are expected. There is still real work to be done to get inflation back to the Fed’s 2 percent target—but the data shows that we’re heading in the right direction for now.

While there are still very real risks that should be monitored, continued economic growth and market appreciation is likely as solid economic fundamentals should help support markets over the longer term.

Since potential for further short-term uncertainty remains, a well-diversified portfolio that matches investor timelines and goals is the best path forward for most investors. As always, you should reach out to your financial advisor to discuss your current plan if you have concerns.

The Takeaway

- Updates in June were largely positive, setting the stage for a strong second half of the

- Over the long run, the outlook remains encouraging, with potential for short-term setbacks